Electricity and Energy Sector Plan: an opportunity to see the big picture

ENA has long advocated a ‘whole of system’ approach to decarbonisation policy, recognising that a narrow focus on specific parts of the system will leave us blind to the broader implications of decisions. The Department of Climate Change, Energy and Water’s (DCCEEW’s) Electricity and Energy Sector Plan (EES Plan), together with the other sector plans, is an important opportunity to bring the whole picture together in one place.

ENA’s submission to the EES Plan discussion paper focuses on the benefits of decarbonisation across the whole energy system. In short:

- Our collective focus must be on decarbonising the whole energy and broader economic system at least cost to meet net-zero emissions targets, with the greatest impact being in decarbonising the electricity, transport, and heavy industrial gas sectors.

- Removing coal from the electricity system is critical, including our focus and commitment to building new transmission and connecting renewables and new firming capacity. More can and should be done on the distribution grid to host renewable generation, facilitate flexible demand measures from smarter customer energy resources (CER) and provide critical storage infrastructure through community batteries.

- The path to decarbonise the light vehicle transport sector by incentivising EVs and facilitating their charging infrastructure is also a next step to decarbonise our economy. Energy networks are critical platforms for the effective roll-out of EV infrastructure and storage needed across the grid.

- To ensure a future for heavy industry in Australia, our initial focus should be to develop a pathway to renewable gas for industry, leveraging the critical role of gas networks in that pathway. Policy decisions to decarbonise the gas sector must fully consider the broader implications for the whole system.

These themes will be unpacked further, below.

1. Decarbonisation is a once-in-a-century opportunity

Decarbonising Australia’s economy is the defining challenge of our time. It is also an unparalleled opportunity. Decarbonising at the least cost will leverage our natural resource advantages, positioning Australia as a leading competitor and provider of choice for a global economy that is also decarbonising.

Policy choices must be made in an integrated, whole-of-energy system context to decarbonise the economy at the lowest cost. A well-coordinated policy approach reduces the risk of excessive costs, higher emissions, and unintended impacts on energy consumers and the economy.

Data suggests we can make the greatest emissions reductions by removing coal from our grid, replacing our fossil-fuel light vehicles with electric vehicles (EVs) and solving for industrial processes that rely on high-heat manufacturing or use gas as feedstock.

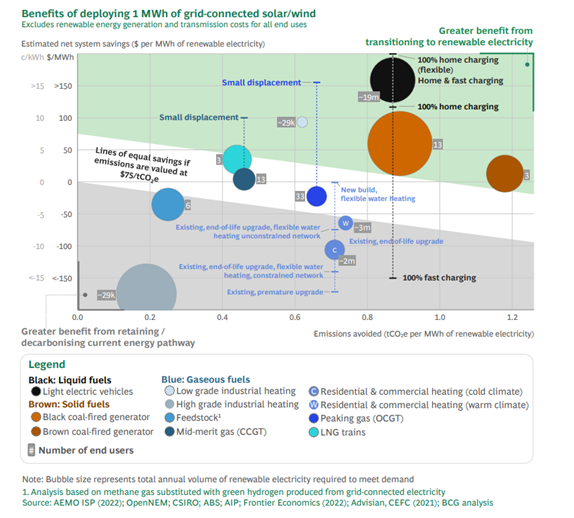

A useful exercise to inform the economy-wide decarbonisation challenge is to consider the costs and emissions benefits from decarbonising by replacing activities with firmed renewable electricity. This question was posed in a recent Boston Consulting Group report, with its key findings shown in the figure below.

In this figure, the size of the bubble indicates the volume of emission that could be reduced in the sector, the position on the X-axis indicates the emissions intensity of the activity, and the position on the Y-axis shows the net system savings from replacing that activity with firmed renewable electricity.

The BCG analysis highlights that:

- Coal-fired electricity generation (the two brown bubbles) is the sector with the most significant volume of emissions with the greatest emissions intensity that can be replaced by firmed renewable electricity with high net system savings

- Light vehicle transportation (the black bubble) is the sector with the next largest volume of emissions with high emissions intensity. This activity also has the highest net system savings when replaced with firmed renewable electricity

- Transitioning gaseous fuels (all the other bubbles) to firmed renewable electricity is a more complex story. The most significant volume of emissions from gas comes from high-grade industrial heating and feedstock, which are moderately emissions-intensive and are costly or unable to be replaced with firmed renewable electricity. Other uses of gas fuels (such as household uses) represent smaller overall sources of emissions and have varying cost and emissions intensity implications.

The critical takeaways are that it makes sense, based on what we know today, to rapidly decarbonise electricity generation and light vehicle transportation by transitioning these to firmed renewable electricity. In contrast, the best approach to decarbonising the gas system is less clear. Decarbonising the gas system will require the development of a thriving renewable gas sector that should initially focus on decarbonising industrial gas use, which has the most significant emission reductions that can be achieved.

2. Unshackling the electricity grid from coal

Removing coal from Australia’s energy mix has been a long-term focus of decarbonisation policy. Strong signals across state and federal governments now provide a long-term direction that Australia’s coal-fired power stations must progressively exit the electricity system and be replaced by firmed renewable generation. It is big job with a tough road ahead, and networks are up for the challenge. The transition away from coal generation in the electricity system is supported by:

- Both electricity transmission and distribution networks connecting utility scale renewable generation across their existing footprint, building new lines to allow renewable power to flow to where it is needed, and keeping the lights on by providing services that are lost as coal generators retire

- Networks building renewable energy zones to connect record volumes of firmed renewable electricity, and

- Distribution networks supporting increased hosting of renewable electricity and storage and playing a pivotal role in facilitating the flexible electricity consumption required to keep system costs down for customers.

This work must continue at pace. We should continue to look at evolving critical regulatory arrangements so they are fit-for-purpose both during and after the transformation. This should include considering how distribution networks can better support the roll-out of storage that captures and stores renewable energy and with the right tariff structures, can make green energy more affordable and within everyone’s reach, no matter their means.

Electrification to decarbonise only makes sense if our electricity supply is largely renewables based, and if coal is removed from the system.

Uniting the nation on the pathway to build the transmission and storage infrastructure is critical to a successful transition. By coming together now, we can unlock the affordable and sustainable future that renewable energy offers us for generations to come.

3. Highway to electric vehicles

The decarbonisation of the transport sector is a massive opportunity for energy customers and should be considered part of the home’s decarbonisation journey. EVs for light vehicle transport will play a significant role in the decarbonisation of the transport sector. The effective decarbonisation of this sector relies on:

- The continued decarbonisation of the electricity system, and

- The use of smart incentives and approaches to ensure that EVs soak up excess renewable electricity and do not materially extend or increase fossil fuel generation.

The efficient integration of EVs into the electricity system will help spread costs across greater electricity consumption, reducing electricity prices in the long run. Our analysis shows that combined household energy bills (electricity plus liquid fuels for transport) are significantly lower when a customer transitions to an EV. A customer’s home decarbonisation efforts are well progressed by replacing a petrol or diesel vehicle with an electric vehicle when they can do so.

Electricity networks are preparing for this change to the use of the grid and have trials underway to explore how to manage demand, incentivise behavioural change and find effective ways to use EVs to soak up excess renewable electricity as it comes online. Regulatory reform could help electricity distribution networks turn these trials into general practice, ensuring critical infrastructure arrives in time, or ahead of the curve, for when and where customers need it.

4. Renewable gas delivered by networks is needed to keep industrial jobs in Australia

Australia must continue to refine materials and manufacture goods. Around 40 per cent of Australia’s gas use occurs in manufacturing and industry, compared with about 10 per cent used in homes. The emissions for many applications in the heavy industrial sector are either impossible or too expensive to abate through electrification. The scaling-up of renewable gases, such as bio-methane and hydrogen, must occur quickly for this sector to survive and thrive.

The sheer scale of industrial energy consumption presents opportunities for policies to deliver investment in renewable gas technologies. This can help drive innovation, reduce costs through economies of scale, and accelerate the development of renewable gas infrastructure and supply chains while keeping Australian jobs on shore. Existing gas infrastructure is a critical platform to enable a nascent renewable gas industry, and for the successful and reliable delivery of renewable gas at scale.

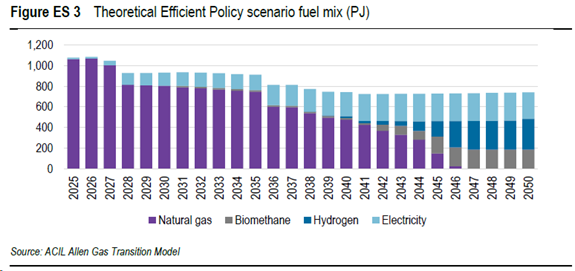

ACIL Allen modelled the lowest cost pathway to reduce emission from gas used by Australia’s industrial, commercial and residential sectors. The model selected the most cost-effective solution for industrial, commercial or residential customers within a carbon budget constraint. The most effective cost solution considered the capital upgrade of appliances, their lifetimes and efficiencies and the fuel cost over the expected life of the appliance. The carbon budget is roughly a linear decrease to 2050 and aligns with the emission reductions outlined in the revised Safeguard Mechanism.

The main results from the modelling show that:

- Both electrification and renewable gases have a role to play in the lowest cost pathway to decarbonisation

- Energy efficiency improvements from electrification reduces the total demand of energy needed to deliver the same services, and

- Early opportunities centre on electrification in some industrial processes (mainly conversion of LNG trains that are undergoing capital equipment upgrades) and later opportunities require renewable gases. This shows that difficult to abate sectors are decarbonised at a later stage as it is more expensive to do so.

Innovative projects to get renewable gases to industry are already in operation. While this renewable gas flows to all customers on the local network, it provides opportunities for industry to purchase renewable hydrogen and biomethane to displace natural gas. Certification and recognition of these emissions reductions from renewable gases is urgently needed to kick-start the development of a renewable gas industry.

The public debate needs to correct away from a narrow lens of gas versus electricity for households, especially while coal is in the system, which reduces the emissions benefit in switching. Instead, there is a growing urgency for renewable gas solutions for industry to address larger-scale energy consumption, reduce significant emissions, and support economic and environmental sustainability on a broader scale. And until we better understand the future of heavy industry currently relying on gas network infrastructure, we should be mindful of any policy that could inadvertently rule out this pathway.

5. A fair transition for all Australian families

At the heart of our transition is every Australian home, and customers can and want to participate in the transition in a meaningful way. It is on us to ensure we don’t leave anyone behind.

Australian households should be encouraged to continue to make choices to decarbonise their homes in ways that suit their needs and the needs of the broader energy system and its users. Australia has some of the highest rates of installed rooftop solar and customers want to continue to be a part of the solution to reducing emissions.

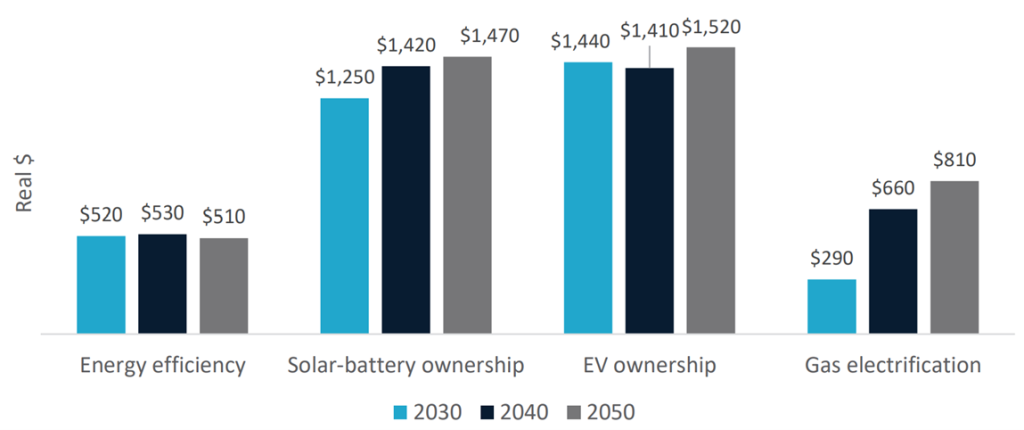

While individual circumstances will vary, research consistently shows that the best ‘bang for buck’ to decarbonise households starts with rooftop solar, energy efficiency practices and purchasing an EV. The cost implications for households are highlighted by research conducted by CSIRO and Dynamic Analysis for Energy Consumers Australia (ECA), with key cost savings by technology and timeframe shown in the figure below.

The greatest near-term benefits come from EVs, solar and batteries, and energy efficiency. (Note that while this research considered solar and batteries together, the value for customers is higher for solar PV than behind the meter batteries, and the value to all users of the energy system is much greater from larger ‘community’ scale batteries installed in front of the meter.) We support ECA’s key policy recommendations from this research that:

- Households need the right information at the right time from a trusted source that is clear and, in their language, to empower them to make decisions that are right for their situation, and

- Households that face barriers to electrifying their homes will need support so that no one is left behind, so that the last households to electrify (which we take to include solar, EVs and energy efficiency) are the ones that choose to wait, not those who could not afford to.

Governments market bodies should pay close attention to the equity outcomes inherent in the decisions they make. Several factors are important to consider:

- Whether a policy is appropriately targeted. For example, a scheme or arrangement to incentivise the uptake of a particular technology type could disproportionately benefit those with sufficient capital to co-invest, leaving behind those without.

- Who pays for a policy. For example, a policy could be paid for by electricity customers (which disproportionately impacts vulnerable customers) or by taxpayers, which can be a more progressive funding source to achieve a policy outcome.

- When customers pay for infrastructure. For example, some long-lived infrastructure assets could reduce in utilisation over time and new infrastructure may require higher cash-flow requirements in early years to ensure they can be financed. Careful thought is required to balance when customers pay for infrastructure and why, so that customers’ long-term interests are promoted and broadly aligned with when they benefit.

Any support for household emissions reductions should be targeted at those most in need and initially at the improved efficiency, solar and EV applications that will make the biggest difference for customers. Electricity and gas networks support helping customers to make decarbonisation choices that are best suited to them, at least cost. There is no one-size-fits-all solution. Individual circumstances and broader impacts on the energy system must be considered, including location, budget, and home type.

Working together, a whole of energy system and economy approach is the right prism in which to navigate a rapid, fair and affordable decarbonisation of the economy.