A Hitchhiker’s Guide to Interest Rate Changes and the Rate of Return

In the Hitchhiker’s Guide to the Galaxy, the answer to the meaning of life, the universe, and everything was simple – it was 42. With some symmetry, in about 42 days we will learn another important answer – the Australian Energy Regulator’s (AER) final approach to estimating the allowed rate of return for around $100 billion of energy network infrastructure over the next four years.

This low-profile number, developed over a process spanning two years, has a claim to be one of the most consequential regulatory settings in the Australian energy framework. Past rates of return have been historically low due to falling bond rates, so what does the situation look like today?

Don’t Panic – a guide to why bond yields matter

Government bond rates are the essential ‘base ingredient’ for the AER’s rate of return settings, and so changes to bond rates are a critical influence on the estimated rate of return.

The rate of return at its broadest level can be thought of as comprising the ‘risk-free’ bond rate, and a ‘risk premium’ designed to reflect the premium required to bring forward required debt and equity financing.

Changes to bond yields play an especially important role in setting the cost of equity, because debt costs are set using a ‘trailing’ historical average that moves only slowly to reflect prevailing rates. [i]

In turn, the rate of return plays a critical role in the setting of network charges that are ultimately passed on to consumers. It impacts the level of investment networks can attract and the energy decisions of consumers, and others seeking to connect to the grid.

The great question – what have low bond yields meant?

When the AER’s early rate of return review process started in mid-2020, government bond rates were close to the lowest experienced since Federation, with the 10-year rate at around 0.9%.

Reviewing these conditions at the time, the regulator agreed that Australia was in a low interest rates environment.

Since that time, interest rates have risen, raising the question: what does this mean for the rate of return approach being determined by the regulator through the review?

The substantial declines in interest rates prevailing across the period since the establishment of national energy network regulation to 2021 has delivered billions of dollars in lower prices to consumers, as lower financing costs were recognised and rightly passed through.

The backward-looking ‘trailing average’ approach to setting debt financing cost means these benefits will continue to be realised in future years, even as wholesale energy prices have recently surged.

So long, low rates

The recent rises in government bond rates and interest rates generally have brought about a sharp departure from historically low rates.

This will, over time, bring upward pressure on network charges, with the return on capital component of charges typically representing the single largest element of network prices.

This upward shift has led some to question whether the AER should have regard to increases in interest rates in setting their rate of return approach.

But before this step is contemplated, it should be established where recent increases in bond rates actually place us.

For a moment, nothing happened. Then…nothing continued to happen

Humans are in a sense naturally prone to notice movement and changes, rather than absolute levels.

It is therefore sometimes easy to miss the fact that while the path to today’s interest rates and bond yields has been steep, their current levels are, historically speaking, entirely unremarkable.

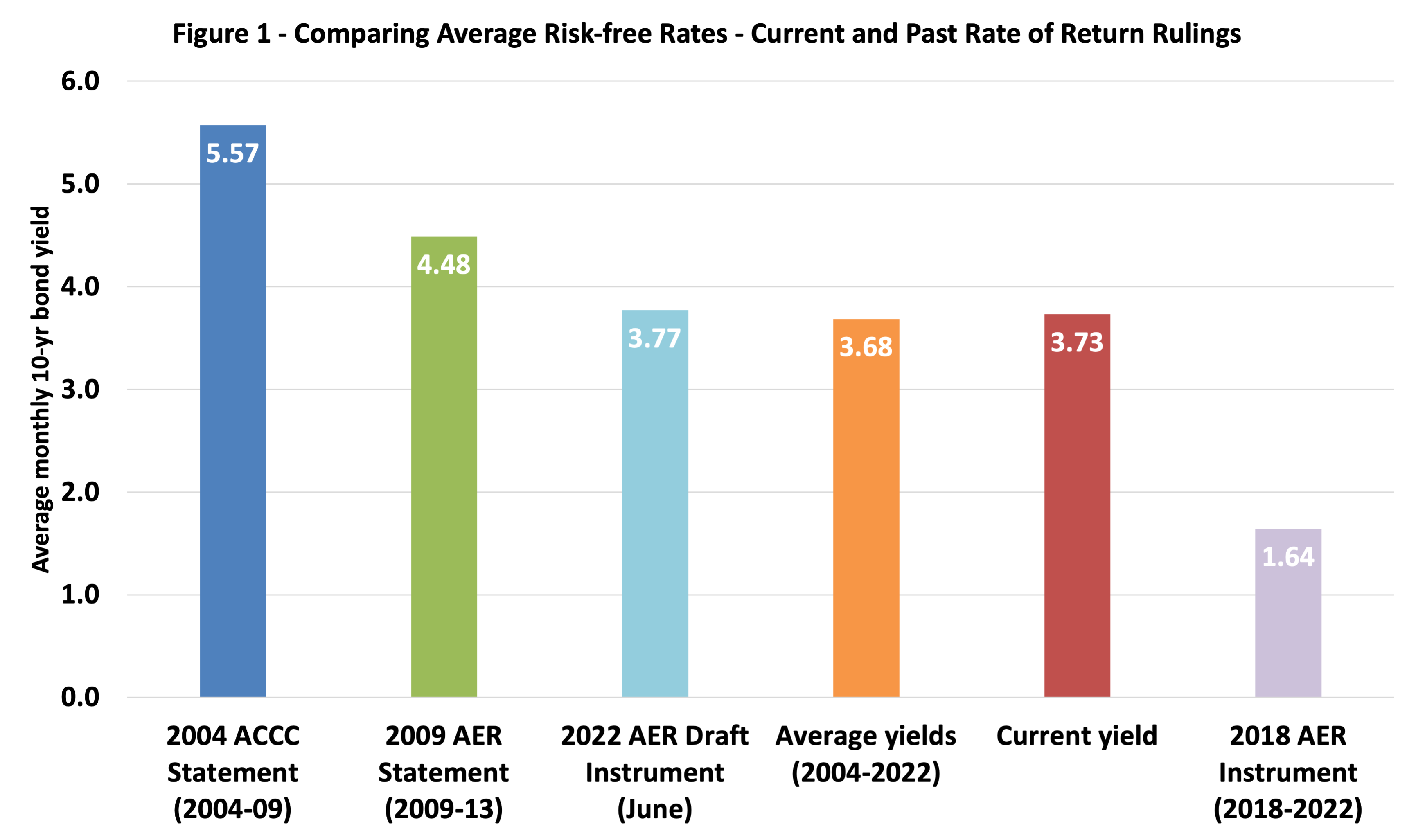

Figure 1 below sets out the average government bond yield across the past two decades.

Source: RBA, Bloomberg; current yield as at 2 November 2022

The bars in this chart map out the average level of bond yields in previous periods covered by current and previous rate of return guidelines, instruments or statements applying to energy network infrastructure.

From this graph, a few facts are evident:

- Interest rates were much higher for many past rate of return rulings – The average bond yield across two previous rate of return rulings (the dark blue and green bars – in 2004 and 2009) were much higher than current yields (in red);

- There is nothing unusual about current bond yields – In fact, the current yield sits extremely close to the average since 2004;

- The outlier experience was the low yields under the previous 2018 Instrument – Network determinations across the last four years locked in bond yields which were well below historically normal rates (light purple bar).

This highlights that the real issue with interest rates is the process of reversion from historically low rates to historically normal rates.

There may be somewhat further to go – the Commonwealth Treasury, for example, adopts a baseline assumption of just over four per cent for its long-term scenario analysis of government financing costs.[ii]

Yet that too is just a projection based on assumed long-term historical averages. In reality, the future path of interest rates has proved to be one of the least predictable settings in the economy.

Seeing bond yields close to levels that have prevailed across the two decades, however, should not be surprising, and is not a clear cause for any particular response in the rate of return context.

Rather, it should remind us to glance at the advice on the cover of the Hitchhiker’s guide: don’t panic!

[i] Allowed regulatory returns are linked to bond yields on the basis that this reflects the changing costs of financing network investments and activities over time, with regulation having the goal of ensuring network businesses are able to recover efficient financing costs. The AER has historically adopted an approach which estimates the allowed cost of equity as a fixed premium added to the prevailing 10-year bond yield.

[ii] Commonwealth Budget Paper No.1 Statement 8: Forecasting Performance and Sensitivity Analysis, October 2022, p.247