Balancing the role of competition in the energy transition – the South-West Queensland Pipeline

Australia’s energy markets deliver customers the energy they need every day through a carefully balanced mix of dynamic market forces, competition, and regulation where this is required to promote the long-term interests of customers.

In the area of gas pipelines, policymakers have provided the scope for the Australian Energy Regulator (AER) to play a key role in choosing that balance – through a power to undertake reviews into the precise ’form’ of regulation that should apply to pipelines.

In the balance…the full regulation or the alternatives

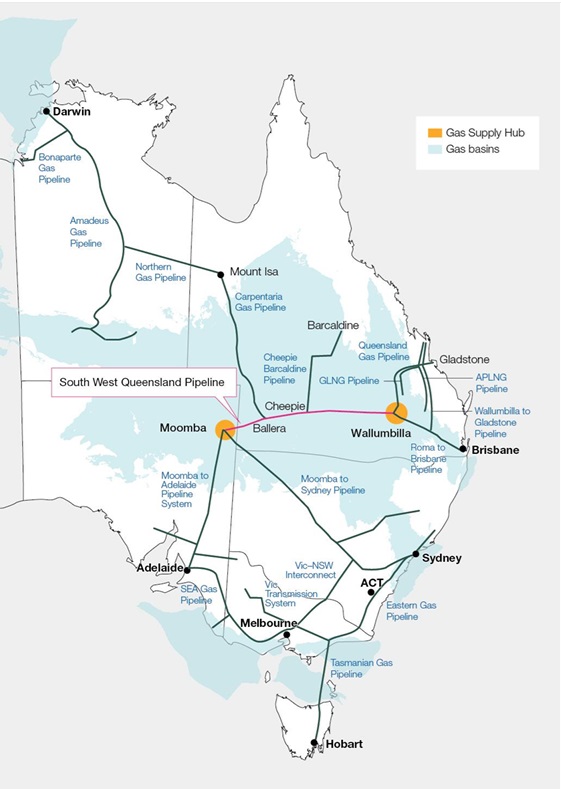

This week, the AER released one of the most significant determinations about the role that regulation and existing competitive forces should play for one of Australia’s most important pipelines – the South-West Queensland Pipeline (SWQP). This pipeline links Queensland and southern gas markets, as well as playing a role in supporting Australia’s LNG export industry.

The South-West Queensland Pipeline and the Eastern Australian Gas Market

Source: AER Discussion Paper, March 2024, p.11

At issue was whether to continue to rely on the open access ‘light regulation’ framework currently in place, or whether the AER should move to impose ‘full regulation’, which includes the effective setting of prices and terms of service by the regulator.

In its draft decision, the AER has chosen to not move towards the imposition of full economic regulation, highlighting that:

- there are a range of constraining factors to mitigate any market power present, and

- the benefits of full regulation are uncertain, and are likely to be outweighed by the costs.

Importantly, the decision recognises that the SWQ has operated since its commissioning as an ‘open access’ pipeline, with its terms of access originally set through a Queensland Government-run competitive tender process.

The road to full regulation: neither simple nor fast

Practically, this history means that movement to ‘full’ regulation for a pipeline which had its initial tariff pathways established by a tender process, would be likely to be a complex, costly, and lengthy regulatory process.

In particular, it would require the development and assessment of a ‘regulated asset base’ (or ‘initial capital base’), and estimation of other ‘building block’ revenue elements such as expected capital, operating and depreciation costs for a pipeline which has operated as a commercially operated pipeline since commissioning.

This would need to be accompanied by the development of a proposed regulatory Access Arrangement informed by pipeline customer engagement, and settlement of that through the substantial established process set out in the National Gas Law and Rules.

The development and settlement of these arrangements for comparable pipelines under the original gas access regime typically required detailed analysis, consultation and assessment over multiple years. In fact, the average time taken for the establishments of the first regulated access arrangement for similar transmission pipelines is just under 2.5 years, with a substantial proportion taking longer – between 3-4 years.[i]

Investment risks of imposing full regulation on a critical link for the transition

In a case where the AER moved to determine that full regulation should apply, this would create the likelihood of pipeline owner and operator APA Group, its owners and investors, and pipeline users having little certainty or clarity about the prices, terms and conditions of access until 2027 or later.

Under this scenario, this regulatory uncertainty would be likely to defer any substantial investments in capacity expansion projects until beyond this date and also have a chilling impact on any privately funded capacity expansions ahead of expected increased demand for SWQP services.

The positive draft decision helps avoid the risk that this form of regulation review will have the ‘on the ground’ effect of derailing timely investment decisions around capacity expansions on the pipeline which will be needed to help support the achievement of the optimal pathway set out in the Australian Energy Market Operator (AEMO’s) 2024 Integrated System Plan (ISP).

This risk would have arisen from the potentially lengthy delays to further investments in pipeline capacity that would underpin the expansion in renewable generation across southern Australian states and territories.

There is no disagreement that under both AEMO’s and other market participants’ projections there will be an increasing need to transport gas from Queensland to meet supply shortfalls, driven by reduced production and declining gas reserves across southern Australian markets.

Both the AER and AEMO’s plans have rightly highlighted the central role that gas transportation services provided by the SWQP will play in supporting gas-fired generation that underpins energy security, customer reliability and lower prices in cases and at times where renewable generation is not sufficient.

Avoiding a regulatory ‘gridlock’ for gas markets

A range of recent modelling assessments have also reinforced the essential role of sufficient pipeline infrastructure capacity and timely expansions to underpin a stable and least-cost transition. AEMO’s 2024 ISP highlights the specific risk that during periods of peak electricity and gas demand, gas supply to gas-fired power generation may be curtailed by pipeline infrastructure constraints.[ii]

Prior to this week’s decision, APA indicated a pause to any capacity expansions for the East Coast gas grid, due to the uncertainty, and there has been public guidance to the same point from existing APA investors.

The AER decision has carefully assessed the likely impacts of moving the SWQP to a new form of regulation, including the potential for the uncertainty generated by any such change to defer or delay capacity expansions which would better allow gas-fired generation to serve as essential back-up to expanding renewable sources.

The draft outcome released this week represents a regulator making a balanced decision that properly weighs the complexities of balancing market and regulatory outcomes through the transition. By avoiding regulatory gridlock being imposed on one of the most critical links in the Australian energy market, just at the moment where a clear investment environment and capacity to adapt will be essential, the AER has helped market outcomes best serve customers through the energy transition, by helping secure reliable support to growing renewable sources.

[i] See Table 4.2 Productivity Commission Review of the Gas Access Regime, Final Report, p.150

[ii] AEMO, Draft ISP (December 2023), p.66