Rise of the machines: will electric vehicles dominate the future?

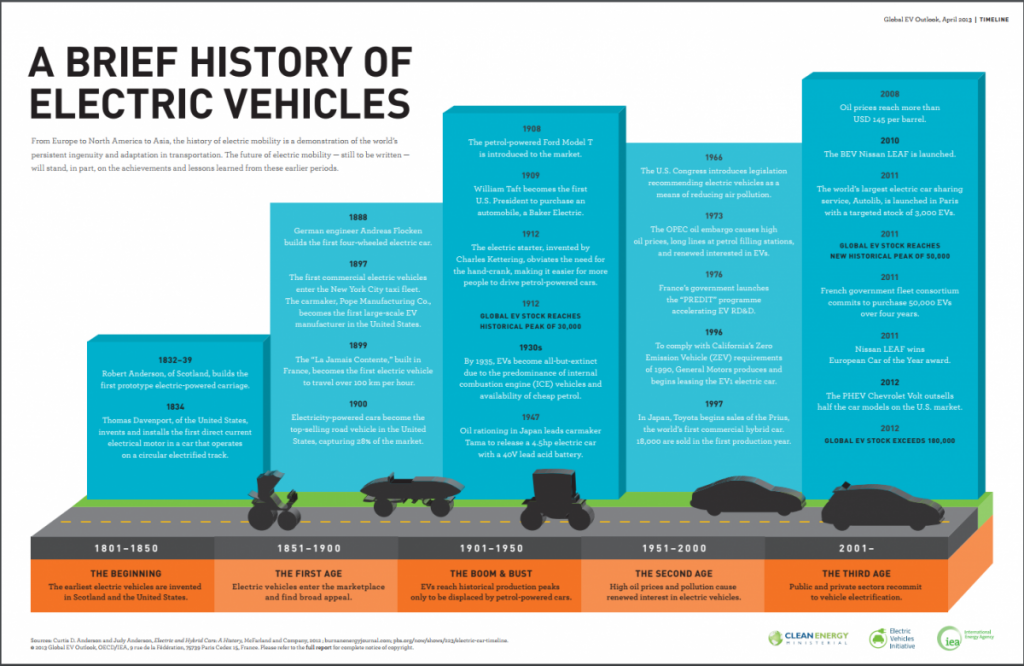

Another battle for industrial supremacy predated the war of currents of the late 1800s – the competition between steam, petrol or electric vehicles.

In 1900 electric vehicles enjoyed their heyday; 28% of all 4,192 cars produced in the US in 1900 were electric and the total value of electric cars sold was more than that of petrol and steam powered cars combined in that year.[1] Even 117 years ago, electric cars won appreciation as quiet, easy to drive, less polluting and being suited to short trips around the city. As more people gained access to electricity in the 1910s, it became easier to charge electric cars, adding to their popularity.[2]

It was a ‘false dawn’ however. The introduction of the mass-produced and “gasoline” powered Model T Ford was a category killer. By 1912, the petrol car cost only $650, while an electric roadster sold for $1,750. By the 1920s the electric vehicle ceased to be a commercially viable product, limited by horsepower, driving distance, and challenged by the ready availability of petrol and better roads. [3] Electric vehicles had all but disappeared in the market by 1935.

http://www.iea.org/topics/transport/subtopics/electricvehiclesinitiative/EVI_GEO_2013_Timeline.pdf

Re-emergence

With the oil crisis in the 1970s, electric vehicles came under a renewed focus, meeting predictable resistance from incumbents. With current global ambitions to reduce carbon emissions escalating in the 2016 COP21 Paris agreement – the prospects of an electric vehicle resurgence are real.

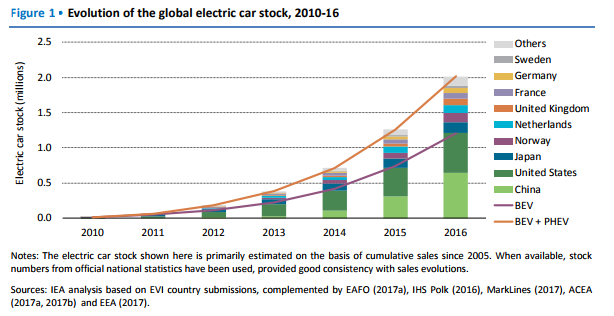

Globally the electric car stock has been growing since 2010 and surpassed the two million-vehicle threshold in 2016. So far, battery electric vehicle (BEV) uptake has been consistently ahead of the uptake of plug-in hybrid electric vehicles (PHEVs).

Norway has achieved the most successful deployment of electric cars (29% market share) followed by the Netherlands (6.4% market share), and Sweden (3.4%). China, France and the United Kingdom all have electric car market shares close to 1.5%. However China was by far the largest electric car market, accounting for more than 40% of the electric cars sold in the world in [4]

Globally, governments are moving to embrace low emission vehicles including electric vehicles (EVs), fuel cell vehicles and gas-fuelled vehicles. Britain recently announced it will follow the French commitment to ban all new petrol and diesel cars and vans. These will be prohibited in the United Kingdom by 2040, France by 2045, with Norway and the Netherlands also banning sales from 2025. India is considering doing the same by 2030.

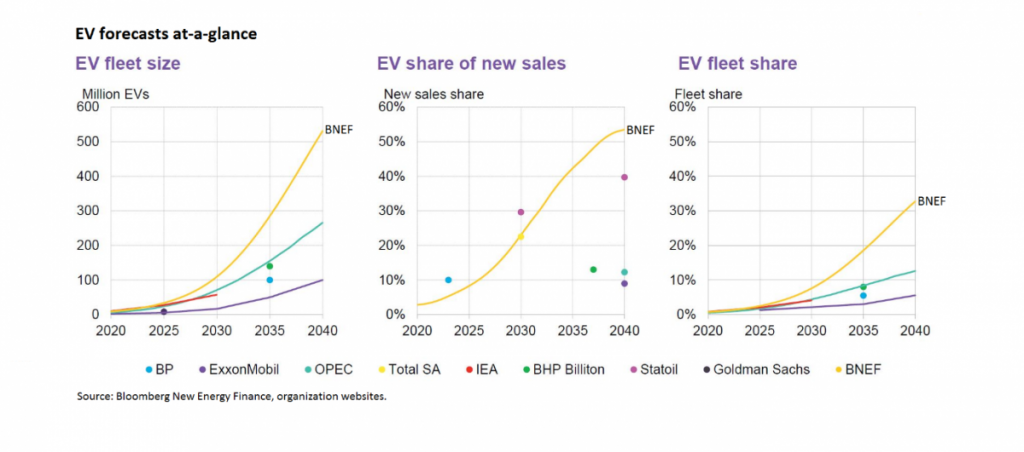

Bloomberg New Energy Finance (BNEF), predicts that by 2040 EVs could account for 530 million out of the world’s 1.63 billion vehicles, or 33%. That was a step up from the 2016 forecast, when BNEF predicted 405.8 million EVs by 2040.

The iPhone moment

Last week Tesla announced the production and roll out of Tesla Model 3 – which will be available in Australia in 2019. Tesla received more than 500,000 reservations for the Model 3 attributed to its base starting price of $US35,000 ($AUD43,700).Tesla has said that the total cost for a fully-optioned Model 3 could reach $US59,500. The costs for the base model in Australia are not yet clear, however buyers could be looking at costs between $AUD50,000 and $AUD55,000 taking into account taxes and charges.

While they may have “iPhoned” the EV – it is not just Tesla getting in on the action.

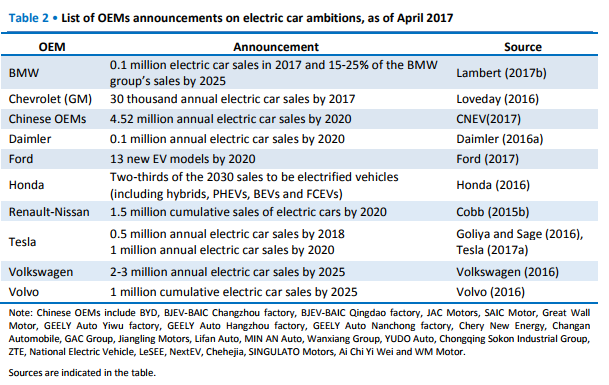

Volvo chief executive Hakan Samuelsson recently announced “the historic end of cars that only have an internal combustion engine.” VW is preparing to launch a hybrid-electric version of the Golf in Australia. Audi and Porsche already offer plug-in hybrid vehicles.

In 2016, Mercedes-Benz chief Dieter Zetsche used the Paris motor show to unveil “an electric product offensive that will cover all vehicle segments, from the compact to the luxury class”.

Cost drives down Australian sales

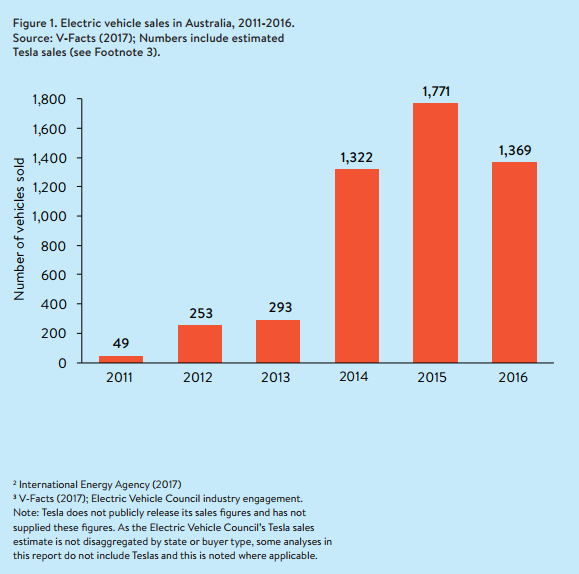

Despite global enthusiasm for EVs, Australian sales fell 23% from 2015 to 2016. Only 1369 electric vehicles were sold in Australia in 2016, representing 0.1 per cent of the market.[5]

The newly formed Electric Vehicle Council (EVC) cites international evidence suggesting a correlation between electric vehicle sales and the number of vehicle models being offered, and that the decline in electric vehicle sales in 2016 may be partially attributable to the low number of models available at less than $60,000.

While the number of electric vehicle models available in Australia has increased over the last six years – with 16 models available for sale in 2016 – the majority of this growth has been in more expensive models. In Australia, 13 of the 16 available models are priced at more than $60,000. Most are priced above $100,000.

Of the three models available for less than $60,000, the Nissan Leaf was only available early in the year, the Mitsubishi Outlander sold out mid-year and the Renault Kangoo ZE is a van that is only available through special arrangement with Renault.

The EVC suggests that an increase in the number of lower cost models available in Australia is likely to increase sales:

“Seven new electric vehicle models and model updates are expected to be introduced into the Australian market in the next 18 months, with three of these expected to be priced at $60,000 or less.”

Connecting the grid to transport

Like its distributed energy stablemates – growth in the uptake of EVs has primarily been driven by advances in technology, such as battery breakthroughs enhancing range and cost reductions.

The Electricity Network Transformation Roadmap examined the effect of EV adoption on the electricity sector under two scenarios:

- Slow change to electricity pricing and incentives; and

- Faster reform of pricing and incentives.

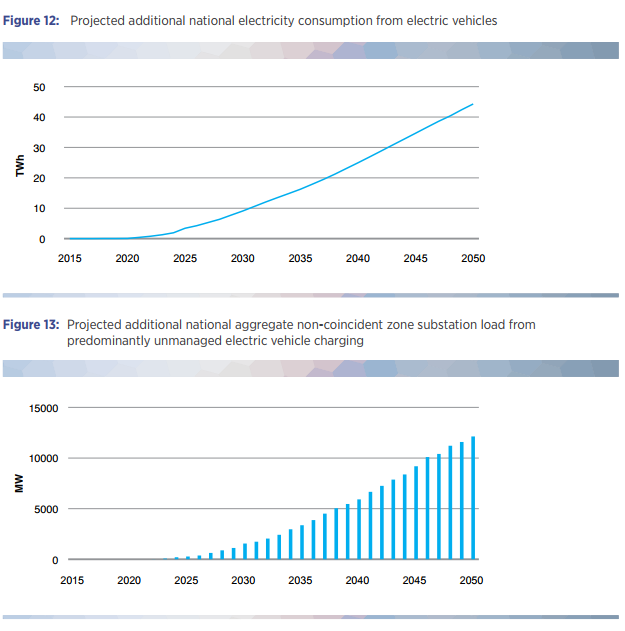

In both scenarios, EVs consumed an additional 5 TWh of electricity in 2027 and 43 TWh in 2050. The impacts on peak demand were very different however. While reformed pricing and incentives minimised the impact of EV adoption, incentivised managed charging, slower pricing and incentives reform added an additional 12,000 MW to non-coincident zone substation peak demand by 2050 due to a higher degree of unmanaged charging (Figure 13).

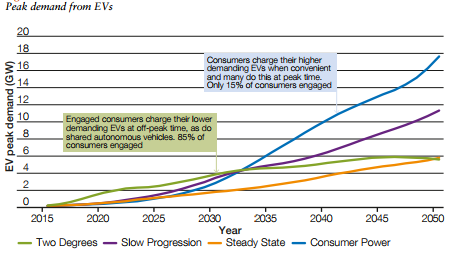

In its recently released annual Future Energy Scenarios report, National Grid suggests that by 2030 there will be between 1.9 and 9.3 million EVs on the roads and if these vehicles were all to charge at the same time it would put significant strain on distribution. If not managed carefully the additional demand will create challenges across the energy system, particularly at peak times.

The report predicts that the growing use of EVs could increase electricity peak demand by 3.5 gigawatts (GW) in Britain by 2030 and that in one scenario without “smart charging” peak electricity demand could rise by 18 GW by 2050. This increase in peak demand would happen where “consumers plug in and start charging their vehicles at their convenience”, ignoring electricity tariffs that are cheaper during off-peak hours. However in another scenario with vehicle sharing and off-peak charging patterns, demand might only rise by 6 GW by 2050.

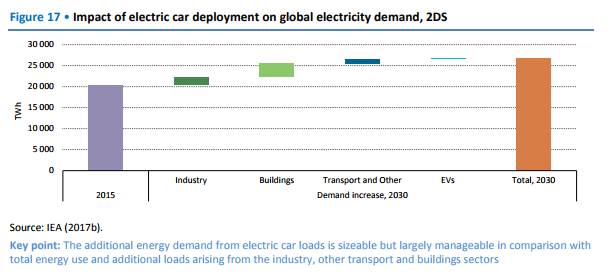

International Energy Agency (IEA) analysis shows the additional energy demand from EV loads is sizeable but largely manageable (IEA, 2017b). The IEA has also identified that rising EV penetration is likely to have an impact on distribution grids in residential or commercial areas first. Because EVs are not stationary, greater understanding of EV charging patterns and technologies will be required to ensure their integration into the distribution grid and to maintain adequacy and quality of power supply, and mitigate the risk of cost increases for consumers.

Like the Roadmap – the IEA recognised that large-scale EV charging and demand response would require optimisation of the energy system and smart management of the relationship with grid infrastructure and EV users. The IEA argued that managing power demand in a world of fast chargers is likely to require the deployment and use of stationary storage at the local or grid level.[6]

To manage this they identify three options for mitigating the negative impacts of EV charging.

Firstly, the buildout of charging infrastructure and deployment at locations and with technologies that minimise negative impacts.

Secondly, incentivising EV uses to maximise self-consumption through solar systems installed on consumers’ homes combined with the available storage and recharging infrastructure.

The IEA suggested that as EV penetration increased, such options could deliver lower costs for both charging infrastructure owners/operators and distribution grids.

However the challenge will be to ensure that existing regulation and price signals provide enough efficiency and flexibility at the system level.

To enable smart charging, regulators and policy makers will have to enable business models that deliver some combination of price signals, control signals and aggregation enabled by data analytics and controls for a large numbers of users.[7]

Finally, as EV penetration increases, charging infrastructure will require common standards and interoperable solutions between charging stations, distribution networks and the EVs themselves.

The future

To date EV market uptake has been largely influenced by the policy environment. As the IEA identifies, key mechanisms currently adopted in leading EV markets target both the deployment of EVS and charging infrastructure.

In the United Kingdom, Western Power Distribution (WPD) has partnered with EA Technology, DriveElectric, Lucy Electric GridKey and TRL for a Network Innovation Allowance funded project – Electric Nation. The project will show how effective demand management using smart chargers is an alternative to network augmentation.

Also in the UK, British businesses now will be able to bid for £20m of government funding for undertaking research and trials of vehicle-to-grid technology. Financial support for energy innovation is expected to double by 2021 and over £600m is already being invested to accelerate the transition to ultra-low emission vehicles. The £20m investment will be awarded to three types of vehicle-to-grid projects.

Institutional support for EVs in Australia has been more slowly realised – however there are still key initiatives rolling out nationally.

The Queensland Government has recently launched the Queensland Electric Super Highway – the world’s longest in one State – supported by Energy Queensland. Once operational this infrastructure will make it possible to drive an EV from the State’s southern border to the Far North. In the initial phase, charging will be available at no cost.

ActewAGL has launched its electric vehicle (EV) charging station network. Eight EV charging stations are operational, powered by 100% Renewable GreenPower. The first installation in the pilot project, a 50kW rapid charger in Greenway in 2016, was the first of its kind in the ACT. Rapid (‘Level 3’) charging stations allow customers to fully recharge their EV in approximately 20 minutes.

In South Australia, the Adelaide City Council will roll out 40 electric charging stations throughout the city in 2017 in addition to the four charging points it currently has in two CBD car parks.

It was concerning to see low emission vehicle policy snared in the politics of ‘carbon taxes’ in recent weeks.

The Ministerial Forum on Vehicle Emissions is currently considering fuel standards, emissions standards and efficiency of vehicles – which may provide more incentives for the take-up of electric vehicles.

While the focus of carbon policy has been on the electricity generation sector, there are also opportunities for decarbonising transport in Australia. The road transport sector accounted for 79 million tonnes of CO2-e in 2015, or 85% of total transport emissions. Light vehicles accounted for 72% of road transport emissions.

The Australian Government’s consultation paper indicates that the proposed model could cut costs to customers by up to $28 billion by 2040 with annual fuel savings for the average owner of a passenger car and light commercial vehicle of up to $519 and $666 respectively.

Australia’s energy transition needs to have clear, long-term objectives that industry and market participants can respond to.

Appropriate fuel efficiency standards can support technology neutral emissions reduction, and better outcomes for customers and the environment – without direct subsidies to particular solutions.

The Ministerial Forum intends to provide a draft implementation plan on potential measures later this year for consideration by the Australian Government.

Given that a whole of economy approach to decarbonisation is required and the significance of efficient carbon abatement in the transport sector, it’s hoped the Australian Government’s policy process will be able to run its course.

[4] Global EV outlook 2017 Two million and counting, © OECD/IEA 2017, p 5

[5] The state of electric vehicles in Australia, ClimateWorks Australia on behalf of the Electric Vehicle Council, June 2017.

[6] Global EV outlook 2017 Two million and counting, © OECD/IEA 2017, p7

[7] Global EV outlook 2017, Two million and counting, © OECD/IEA 2017, pp43-44