What electricity CPI is telling us

The ABS recently released the September quarter 2018 Consumer Price Index (CPI) data which showed overall Australian CPI tracking about where the RBA expected it to be at 0.4 per cent. What’s interesting to the energy price watchers among us is that the electricity CPI measure also comes in at a very modest 0.4 per cent nationally[1]. Does this provide much-needed reassurance that the electricity price hikes of the past couple of years are only visible in the rear-view mirror or is there more to the story?

Diving deeper than the national level, price stability is less than certain. Here’s what electricity CPI is telling us.

At a city level

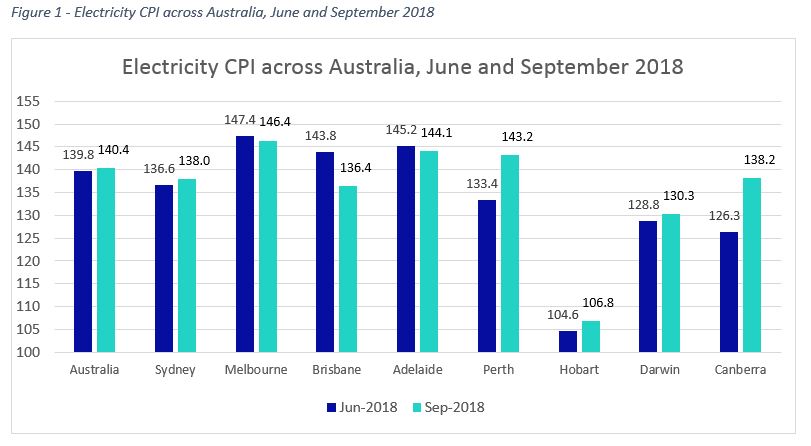

While the national average paints a rosy picture of stable electricity prices, the state capital-specific CPI measures are anything but, with a few cities experiencing large price swings over the most recent quarter.

The regulated retail prices in Canberra and Perth increased under the approval of their respective regulators. The regulators set new prices on 1 July each year, resulting in September CPI showing larger changes in these cities than elsewhere.

The Independent Competition and Regulatory Commission (ICRC) which regulates Canberra’s retail prices, increased them by 3.2 c/kWh off the back of a 1.7 c/kWh increase in wholesale costs and a 0.9 c/kWh increase in green scheme costs. The ICRC approach smooths price changes over roughly two years, citing the rapidly increasing energy purchase costs from mid-2016 to mid-2017 for their increase in wholesale costs. Green scheme costs increased due to the required number of small-scale renewable certificates set by the Clean Energy Regulator more than doubling from the previous year[2].

In Perth, the picture is not as clearly explained as it is in other jurisdictions, owing to retail pricing being more of a political decision with less published documentation outlining the underlying causes of price changes.

Brisbane has seen some much-needed price relief, while in other states there have been either minor increases or decreases barely large enough to make a dint.

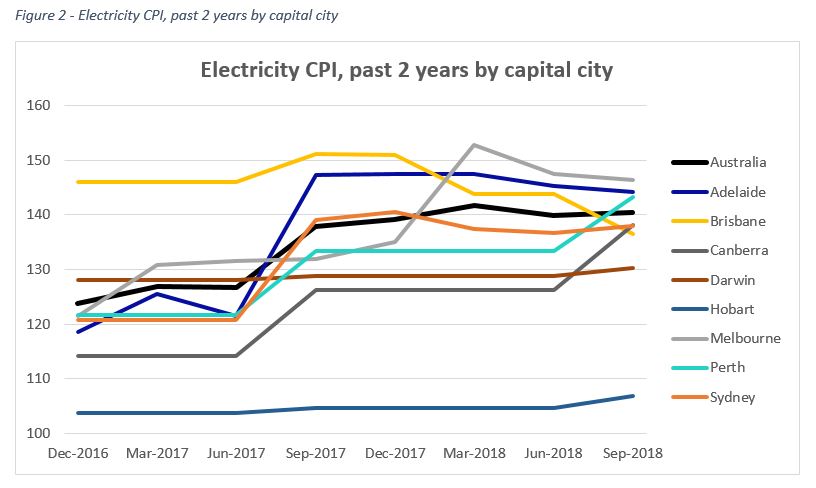

Even with a few states experiencing large swings, the national electricity CPI is still only 0.4 per cent, a hopeful indication that price stability is being maintained in the short-term. Taking a longer term view of the measure reveals the linkage of broader price trends to the timing of Hazelwood’s closure in March last year.

Retailers increased their prices in response to the higher wholesale costs in July 2017 for most of the country and January 2018 for Victoria. The increases correspond with the CPI electricity spikes on Figure 2 in September 2017 and March 2018 for respective non-Victorian states and Victoria.

Beyond Hazelwood’s closure, the underlying causes of price movements across time are difficult to pin down.

Wholesale price data is published by AEMO and provides for the calculation of volume-weighted wholesale costs. However, this isn’t the price retailers actually pay for their electricity because of the futures contracts they’ve entered into often well in advance of the date electricity is actually required. Every retailer has a different portfolio of hedging contracts, so determining their actual costs isn’t feasible.

Similarly, the retail cost portion of a customer’s bill is private and not disclosed publically. The most significant part of the bill where customers have complete information available to them is the network charge.

Network charges and CPI

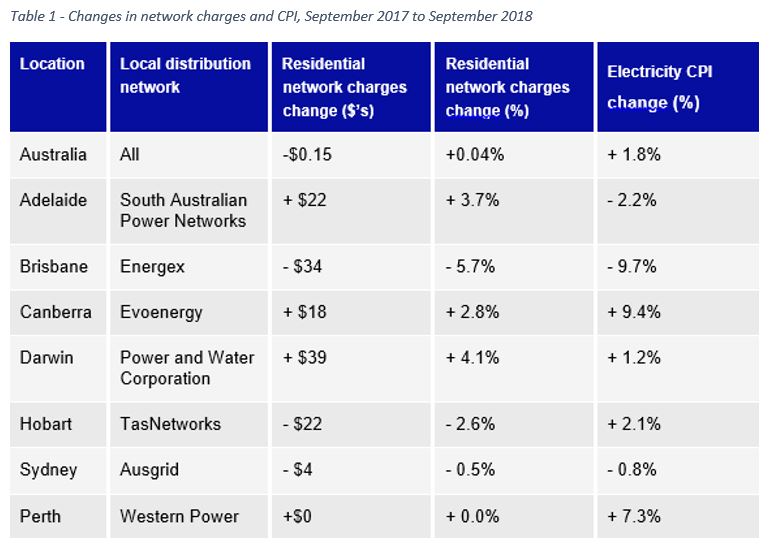

Australian networks outside Victoria change their network prices on 1 July, with those alterations filtering through CPI in the September quarter. Across Australia, the customer-weighted average change in network charges is insignificant, at an increase of 0.04 per cent. Similar to CPI, each city experienced different changes in network costs. Assuming retailers fully pass these through, we can observe the impact that changing network costs have had on electricity CPI.

Major CPI increases were present in Canberra and Perth, with network charges contributing somewhat to the rise in the Canberra. Perth’s network charges were flat and had no effect on price due to delayed regulatory processes.

Brisbane prices were well in decline with networks playing their part, while reductions in Hobart’s network charge did not flow through to price reductions for customers. Network charges have also contributed to the minor price decreases in Sydney.

Darwin’s increase brings its prices to more cost reflective levels while Adelaide’s rise follows significant past reductions, which have meant the 2018-19 charges are $60 lower than 2014-15 charges. In fact, despite the hype about power prices, distribution prices in South Australia have gone up less than CPI since 1999.

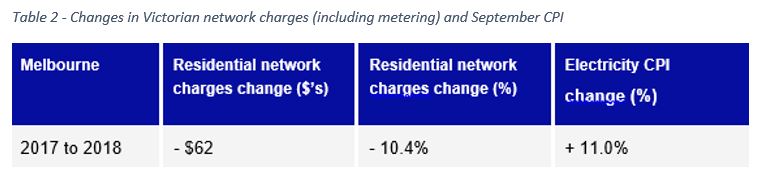

In Melbourne, the full year results also show network prices declining but an increase in overall costs stemming from other parts of the supply chain.

We covered the network price changes coming on 1 January 2019 here.

However, while the overall prices rises have been undoubtedly far less than this time last year, with politicians waving around ‘big sticks’, threatening unprecedented regulatory and market interventions and making plenty of energy-related election promises, future electricity prices are anyone’s guess.